How to use

This User Guide provides guidance on how to use the NCMC like an open library to identify potential natural capital metrics, measurement methods and data sources, which can then be adapted to serve whatever purpose the user requires.

It does not provide overall guidance on natural capital accounting, assessment or reporting; nor does it provide detailed guidance on how to measure natural capital or how to obtain or analyse natural capital data. However, other sources of overall guidance are listed below, and sources of more detailed guidance relevant to each metric are included in the results section for that metric (where available).

The NCMC is a catalogue of potentially relevant natural capital metrics, intended to serve the widest possible range of users. It is not prescriptive – it is unlikely that any single organisation would find all of the listed metrics applicable. Neither is it exhaustive or complete – rather, it represents an initial list of potentially relevant metrics sourced from numerous experts and stakeholder inputs, and which will continually be added to and refined over time. Efforts have been made to align the content and structure of the NCMC with major international standards such as the United Nations System of Environmental-Economic Accounting (SEEA) standards and Taskforce on Nature-related Financial Disclosures (TNFD) Recommendations. However, no single standard covers all possible forms of natural capital measurement, and therefore decisions have had to be made about how to resolve differences between standards, while organising the catalogue in a logically consistent way.

Once a relevant metric has been identified (either through using the search function or navigating the side bar, drop-down menus and tabs), the NCMC typically provides some contextual information about the metric (e.g. metric type and typical units); example measurement methods arranged according to three tiers and including example guidance, data sources and references, where available; and further information in the form of notes.

Step-by-step guide to using the NCMC

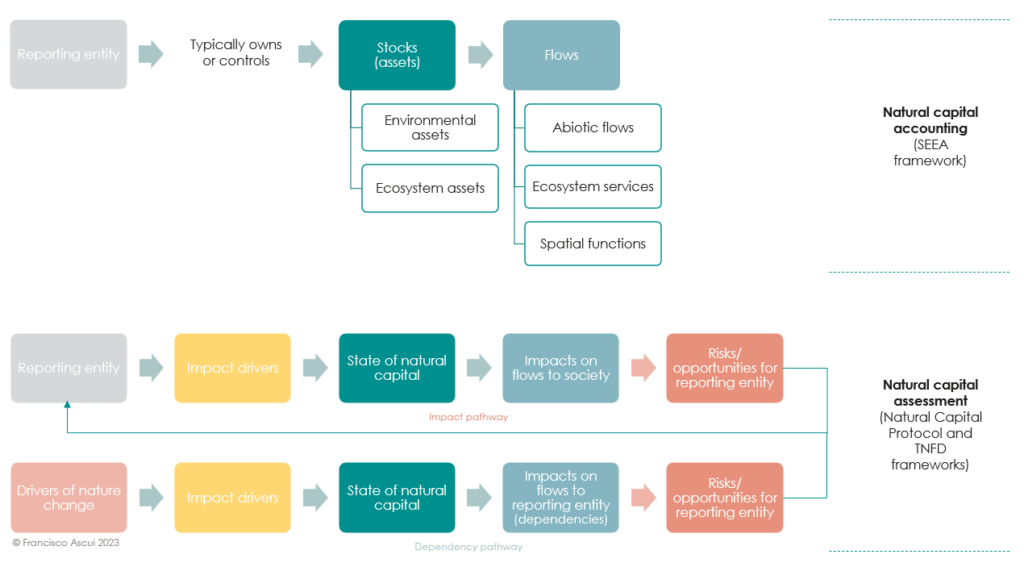

Step 1: Determine which overall section of the NCMC is most relevant to you – Natural Capital Accounting, or Natural Capital Assessment

- If your organisation owns or controls significant natural capital assets, e.g. areas of land or water, then you may be interested in accounting for those assets and the flows of benefits derived from those assets. If so, the Natural Capital Accounting section may be most relevant. This section includes metrics for measuring the quantity/extent and quality/condition of individual environmental assets or components of the biophysical environment (such as mineral resources, land, timber or water) as well as whole ecosystem assets (such as forests, wetlands or rivers) where multiple individual environmental assets interact as a system.

Natural capital accounting is also known as environmental-economic accounting, particularly when applied to the development of national statistics. When applied at a country or regional level, the scope is usually defined by territorial boundaries, whereas when applied at the level of an individual entity, the scope would normally be defined by the entity’s ownership or control. The Natural Capital Accounting section of the NCMC provides metrics to support accounting consistent with the United Nations System of Environmental-Economic Accounting (SEEA) standards. - If you are more interested in your organisation’s relationship with nature, regardless of ownership or control, then the Natural Capital Assessment section may be most relevant. This section includes metrics for measuring an organisation’s impacts and/or dependencies on natural capital. The resulting information could be used to support improved management of an organisation’s nature-related risks and opportunities (arising from its impacts and/or dependencies), or to support disclosures in accordance with Taskforce on Nature-related Financial Disclosures (TNFD) Recommendations, or International Sustainability Standards Board (ISSB) disclosure standards.

- It is possible that both sections may be relevant to your organisation, for example if your organisation owns significant natural capital assets, and also has significant impacts and/or dependencies on nature beyond those assets.

Step 2A: Within the Natural Capital Accounting section, determine which sub-sections are most relevant to you – Environmental assets or Ecosystem assets (or both)

- Environmental assets are individual components of the biophysical environment, such as mineral resources, land, timber or water. These metrics can be used to measure the quantity or quality of individual environmental assets, and the physical or monetary flows of benefits that they provide. The Environmental assets section is aligned with the SEEA Central Framework (SEEA-CF).

- Ecosystem assets are whole ecosystems (complexes of living and non-living, or biotic and abiotic, environmental assets that interact as a functional unit). The Ecosystem assets section is aligned with SEEA Ecosystem Accounting (SEEA-EA). By definition, ecosystem assets may include various individual environmental assets that could also be accounted separately. For example, a forest ecosystem may include timber resources, but ecosystem accounting allows for consideration of ecosystem services that the forest may provide beyond the provision of timber, such as water flow regulation services or air filtration services.

The two sections are not mutually exclusive – they represent different ways of thinking about what is relevant to account for in the environment. A user may choose to account only for individual environmental assets, or only ecosystem assets, or a combination of both. However, if both types of accounts are presented, the information in each should be consistent, and quantities and values for assets that are common to both sets of accounts should not be added together. For example, the value of timber resources should be included in the value of wood provisioning services as part of an ecosystem account for a forest, and therefore not added to the total ecosystem accounting value for the forest.

Step 2B: Within the Natural Capital Assessment section, determine which sub-sections are most relevant to you – Impacts or Dependencies (or both)

- Impacts are a “negative or positive effect of business activity on natural capital” (Natural Capital Coalition, 2016, pp. 16-17). Impacts can be directly caused by the reporting entity, indirect or cumulative (TNFD, 2023). Generally, impacts are caused (or exacerbated by) certain actions, known as impact drivers, which result in changes to the state of nature and its ability to deliver ecosystem services or other benefits to humans. This in turn can give rise to risks (and/or opportunities) for the reporting entity, for example when natural capital that the reporting entity depends on is negatively affected (see next point), or when society responds to impacts by imposing regulation, fines, or constraints on market access.

- Dependencies are “aspects of environmental assets and ecosystem services that a person or an organisation relies on to function” (TNFD, 2023, p, 115). Changes to the state of nature can affect its ability to provide the ecosystem services, abiotic flows (e.g. water or mineral resources) or other environmental conditions (Smith et al., 2023) that an organisation depends on. This in turn can give rise to risks (and/or opportunities) for the reporting entity.

Step 3: Find metrics, measurement methods and data sources

Within the subsection of the NCMC that is most relevant to you, you can find metrics by browsing within that subsection (using the left hand navigation panel), or by using the Search and Filter functions. The Environmental assets and Ecosystem assets subsections are arranged by type of environmental asset, and ecosystem type; whereas the Impacts and Dependencies sections are arranged according to categories of natural capital impacted or depended on.

Note that metrics in the NCMC have been named in a way that is intended to be as generic as possible, noting that the same metric may be called different things in different measurement or reporting frameworks, and there may be many similar metrics which can be considered variations of the generic metrics included in the Catalogue.

Once you have found a relevant metric, the Catalogue provides suggested measurement methods and data sources, arranged into three tiers (see FAQ: What are tiers?). All suggested examples are illustrative and not prescriptive. It is up to the user to decide how to adapt the suggestions from the NCMC to suit their particular context and purpose.

Use Cases

The Catalogue is for anyone and everyone to use – just like an open library.

Natural capital measurement ultimately produces environmental data and information. This can be used for many different applications or use cases, such as:

- developing an inventory of natural capital assets

- assessing the benefits flowing from natural capital assets

- assessing organisational interactions with nature

- State of the Environment reporting

- Environmental impact assessment.

Different types of users are likely to use the Catalogue in different ways. The following examples are indicative and not prescriptive.

Land managers

Users might include agricultural, fisheries and forestry primary producers, as well as companies in any other sectors involving significant landholdings, such as energy, telecommunications and mining. Natural capital is typically relevant to these users due to their ownership of natural capital assets, such as land, as well as through their direct (and potentially also indirect) operational impacts and dependencies on nature.

Benefits

Using consistent metrics from the Catalogue can support land managers to:

- better manage their own natural capital assets

- better manage their direct (and possibly also indirect) nature-related impacts and dependencies, and the associated nature-related risks and opportunities arising from these

- make use of environmental data from public or private environmental data service providers to supplement their own data

- report (if desired) on the state of their natural capital assets and flows of ecosystem services in accordance with the United Nations SEEA standard

- report (if desired) on their nature-related impacts, dependencies, risks and opportunities in accordance with frameworks such as the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD), International Sustainability Standards Board (ISSB) standards, Australian Agricultural Sustainability Framework (AASF) or Science Based Targets for Nature (SBTN).

Governments and NGOs

Users of the Catalogue might include national, state and regional-level government agencies and non-governmental organisations (NGOs) with responsibility for managing natural capital assets, producing environmental-economic accounts or State of the Environment reporting, or managing trusted environmental data and information supply chains.

Benefits

Using consistent metrics from the Catalogue can support governments and NGOs to:

- measure and therefore be able to better manage natural capital assets that they have responsibility for managing

- make use of environmental data reported by other landowners and companies, as well as private environmental data service providers to supplement their own data

- drive increased consistency between environmental data and reporting across and within levels of government, as well as between government, NGOs and the private sector

- support the establishment of trusted environmental data and information supply chains based on the Shared Analytic Framework for the Environment (SAFE).

Corporations

Users might include any type of corporation, but it may be particularly relevant to those with significant indirect impacts or dependencies on nature through their supply chains, such as agricultural, fisheries and forestry processors and manufacturers, retailers and companies in other associated industries, such as fertiliser and agrochemical production or transportation. Natural capital is typically more relevant to these users via their supply chain interactions with primary producers, than through their direct operations or ownership of natural capital assets.

Benefit

If corporations use consistent metrics from the NCMC they will be able to:

- more confidently compare and benchmark the environmental performance of supply chain partners

- develop consistent and comparable nature-related key performance indicators to help improve the environmental performance of supply chain partners and therefore the supply chain as a whole

- aggregate environmental information across supply chains, e.g. to understand net supply chain impacts or dependencies on nature

- understand and therefore be able to manage and report on their exposure to nature-related risks and opportunities, in accordance with the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD).

Financial sector

Users of the Catalogue might include investors and lenders. Natural capital is typically more relevant to lenders and investors via their financial interests in the companies in their investment or loan portfolios, rather than via their direct operations.

Benefits

Using consistent metrics from the Catalogue can support the financial sector to:

- more confidently compare and benchmark the environmental performance of investee companies and borrowers

- develop consistent and comparable nature-related key performance indicators to help improve the environmental performance of investee companies and borrowers

- aggregate environmental information across portfolios, e.g. to understand net financed impacts or dependencies on nature

- understand and therefore be able to manage and report on their exposure to nature-related risks and opportunities, in accordance with the recommendations of the Taskforce on Nature-related Financial Disclosures (TNFD).

Environmental data service providers

Users of the Catalogue might include both public and private organisations involved in the collection, storage and provision of environmental data.

Benefits

Using consistent metrics from the Catalogue can support environmental data service providers to:

- align their data products with metrics used by landowners, supply chains, the financial sector, governments and NGOs

- enhance interoperability between their data products and those produced by others.

Accounting vs Assessment

The main focus of natural capital accounting is on natural assets, and the flows of benefits derived from those assets. When applied at a country level, the scope is defined by territorial boundaries, whereas when applied at the level of an individual entity, the scope would normally be defined by the entity’s ownership or control.

Natural capital assessment considers the reporting entity’s impacts and dependencies on natural capital through the concept of impact and dependency pathways, and may involve any natural capital causally related to the entity through these pathways, regardless of territory, ownership or control. Both impact and dependency pathways involve changes to the state of natural capital (equivalent to accounting for stocks of natural assets) and changes to flows (equivalent to accounting for flows of benefits from natural assets), but they are differentiated according to the principal cause and effect of these changes.

Impacts involve changes caused by the reporting entity, which may ultimately result in consequences for the reporting entity (such as increased regulation, fines or loss of access to certain markets).

In the case of dependencies, changes are typically caused by wider change drivers (such as climate change) which may ultimately result in consequences for the reporting entity due to changes in the availability of flows that the entity depends or relies on.

Importantly, it is not always necessary to fully account for changes in the state of natural capital, or the availability of flows, in order to characterise an entity’s impacts or dependencies. For example, information on an entity’s greenhouse gas emissions (an impact driver) may be sufficient, without also providing a full account of the state of greenhouse gases in the atmosphere. Likewise, information on the availability of essential flows to a reporting entity may be sufficient, without also providing a full account of the state of the natural capital asset(s) that provide those flows (particularly when the natural capital assets in question are now owned or controlled by the reporting entity, it may be unreasonable to expect them to provide such information).

For more help navigating your overall approach to natural capital accounting or natural capital assessment, we recommend accessing CSIRO’s Natural Capital Handbook (Smith et. al., 2023).

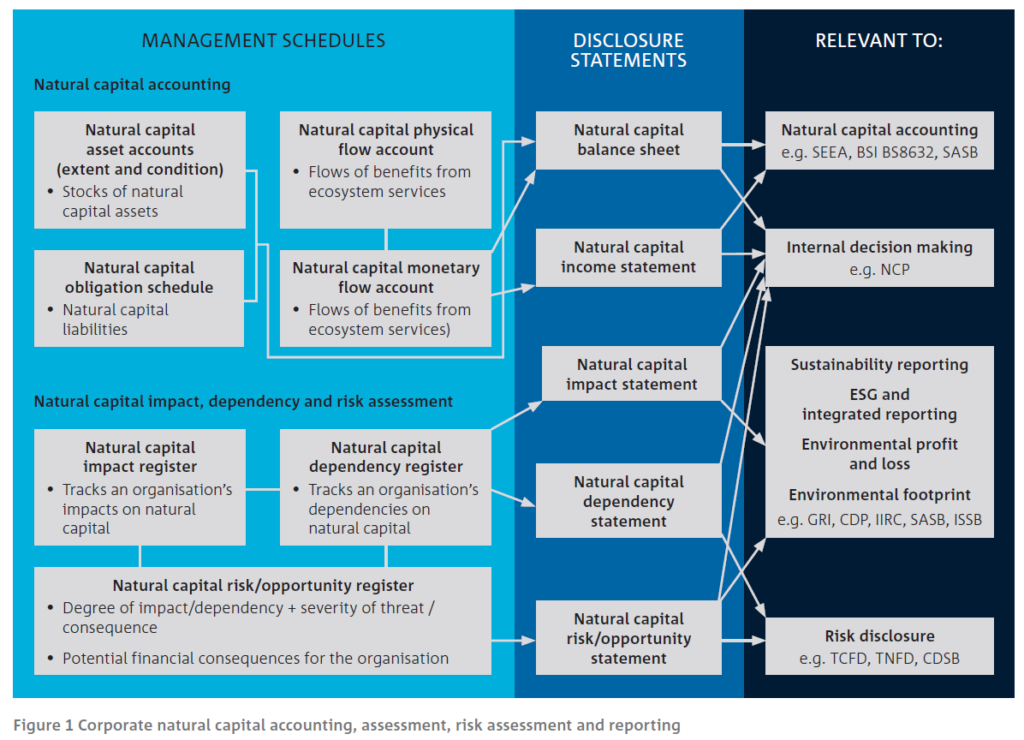

This diagram illustrates some important relationships between natural capital accounting and natural capital assessment.

Tier Guide

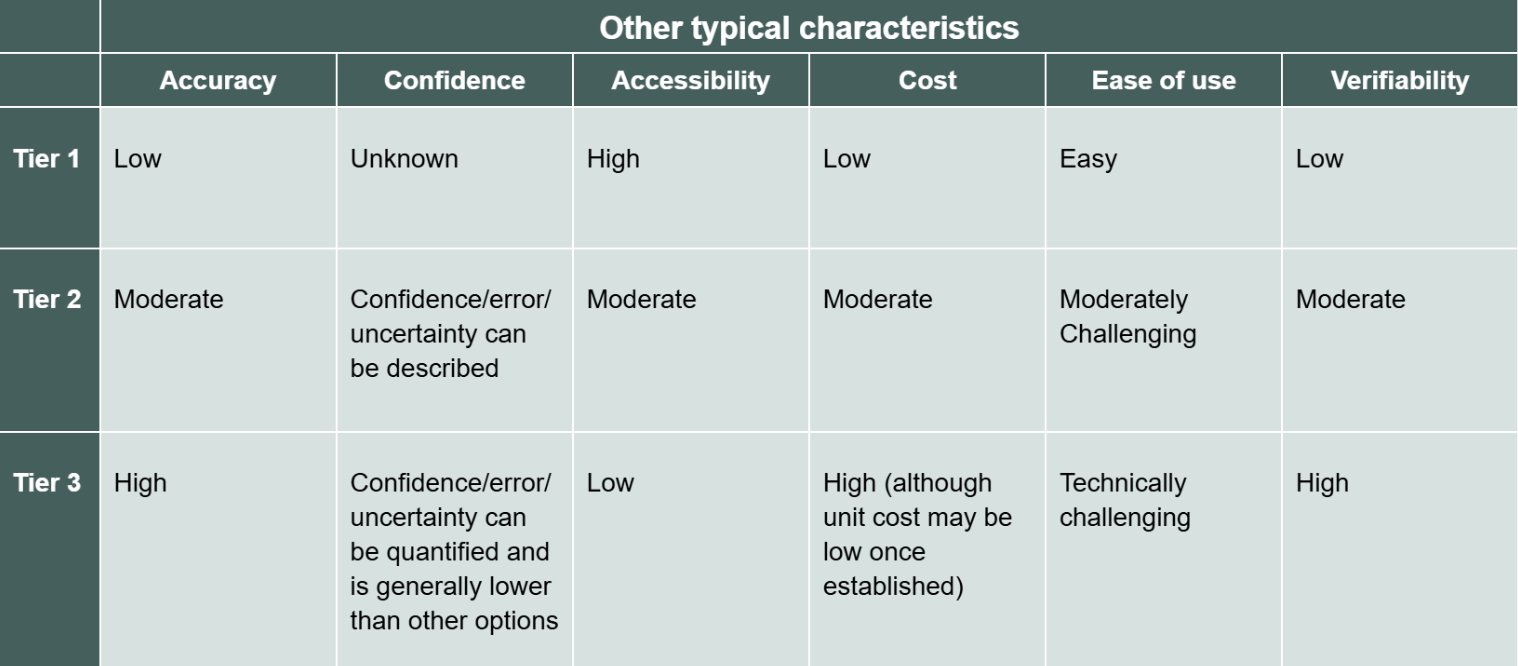

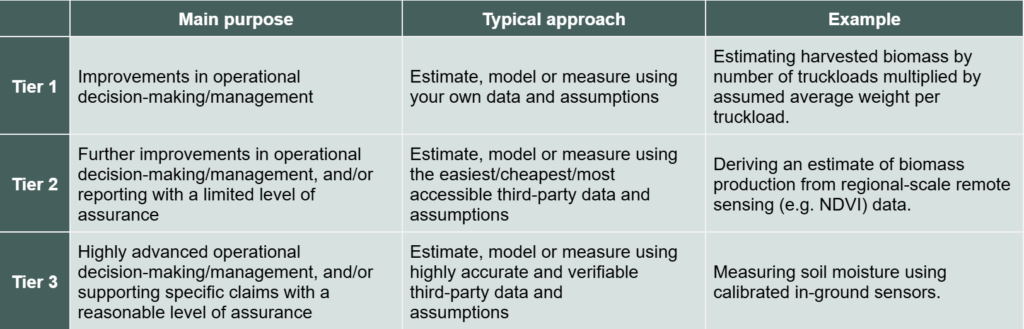

Tiers explanation: Natural capital can be measured in many different ways, by different users for different purposes. The NCMC allocates metrics and methods to three tiers, corresponding to different user needs and approaches to measurement, as summarised in the table below.

- Verifiability, accuracy and costs tend to increase as you move from Tier 1 to Tier 3.

- Confidence/error tends to shift from unknown to quantified from Tier 1 to Tier 3.

- Ease of use and accessibility generally moves from easy through to challenging from Tier 1 to Tier 3.

FAQs

How can I use the NCMC?

The User Guide provides help on how to use the NCMC including use cases, an explanation of key terms, an FAQ and further guidance materials. You can learn more about the NCMC here.

Which international standards and frameworks can the NCMC help me report to?

The NCMC is designed to present natural capital accounting and assessment metrics that are consistent with national and international standards and frameworks such as the United Nations System of Economic-Environmental Accounting (SEEA) and the Taskforce on Nature-related Financial Disclosures (TNFD).

How is the NCMC being developed?

The ongoing technical development of the NCMC is governed by a group of technical experts from CSIRO, ANU, La Trobe University, Griffith University, Federation University, Accounting for Nature and Farming for the Future. These experts have an active interest in advancing the measurement and management of natural capital in Australia and globally.

Refer to ‘About the NCMC for further details.

What are the relationships between natural capital accounting and natural capital assessment?

What are the Tiers?

Natural capital can be measured in many different ways, by different users for different purposes. The NCMC allocates metrics and methods to three tiers, corresponding to different user needs and approaches to measurement, as summarised in the table below.

- Verifiability, accuracy and costs tend to increase as you move from Tier 1 to Tier 3.

- Confidence/error tends to shift from unknown to quantified from Tier 1 to Tier 3.

- Ease of use and accessibility generally moves from easy through to challenging from Tier 1 to Tier 3.

What is the difference between ‘Environmental Assets’ and ‘Ecosystem Assets’?

Environmental Assets are measures for natural assets, relatively easily measured as individual components of the environment that provide economic benefits (e.g. mineral resources, land, timber and water). Covered by the SEEA Central Framework (SEEA-CF) and measured in terms of physical quantity and monetary value.

Ecosystem Assets are measures for the sub-set of environmental assets which involve diverse ecosystems. Ecosystem assets are covered by the SEEA Ecosystem Accounting (SEEA-EA) and measured in terms of extent and condition. Produce flows of ecosystem services which can be measured in physical and monetary terms.

How does NCMC Version 2.0 differ from the Version 1.0?

Version 2.0 includes updates to the technical content of the NCMC and improvements to the website user experience.

All updates were informed by extensive stakeholder feedback on Version 1.0, plus further inputs from Technical Reference Panel members, Advisory Group members, and a range of user experience, website and communication professionals.

Find out more from the ‘About the NCMC‘ page.

Where can I go to access further resources to support my overall natural capital measurement approach?

For more help navigating your overall approach to natural capital accounting or natural capital assessment, we recommend accessing CSIRO’s Natural Capital Handbook.

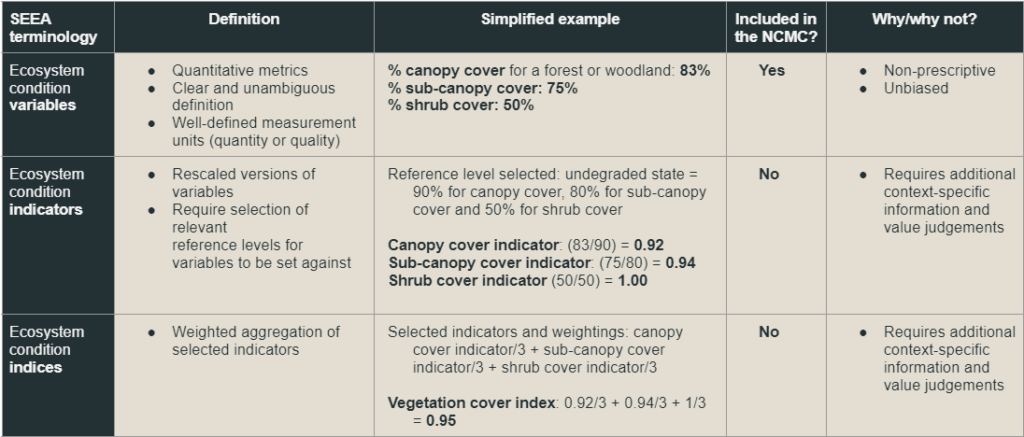

What is a metric vs a variable/indicator/index (SEEA definitions), and how are they included or not in the NCMC?

The following table outlines the SEEA definitions of variable vs indicators vs index (indices) and how they are included or not in the NCMC:

How are metrics, methods and other material selected for the NCMC?

To ensure the quality, integrity and interoperability of the NCMC, metrics, methods, data sources and reference materials are selected to align with a set of NCMC Inclusion Guidelines endorsed by the Technical Reference Panel.

Refer to ‘About the NCMC’ for further details.

Could the Catalogue be used for verification, is it connected with a verification standard?

The NCMC is not a certification framework, so it is up to users to decide if they wish to make any assertions about accounts or assessments based on the NCMC, and whether they wish to have these assertions verified, according to their own criteria or any other certification framework. Users should also take note of any guidance or restrictions on assertions contained in external materials that the NCMC may refer to.

While the NCMC is not a certification framework, it does provide three tiers for measurement methods, which generally correspond with increasing levels of assurance or auditability. Tier 1 usually depends on user-generated data which can be challenging to audit, whereas Tier 3 is associated with third-party instrumentation or data providers that typically produce auditable data.

Is the Catalogue only broad acre or could it extend to forestry?

The catalogue applies to all land use types.

References

Abed, T. and Stephens, N.C. (2003) Tree measurement manual for farm foresters. Second edition, ed. M. Parsons. Canberra: National Forest Inventory, Bureau of Rural Sciences. Available at: https://www.agriculture.gov.au/sites/default/files/documents/Abed_Stephens_Tree_Measurement_Manual_2003.pdf (Accessed: 3 October 2024).

Ascui, F. and Cojoianu, T. (2019) Natural Capital Credit Risk Assessment in Agricultural Lending: An Approach Based on the Natural Capital Protocol. Oxford: Natural Capital Finance Alliance. Available at: https://www.unepfi.org/wordpress/wp-content/uploads/2019/04/Natural-Capital-Credit-Risk-Assessment-2019-2.pdf (Accessed: 3 October 2024).

Brack, C. L. (1999) Forest Measurement and Modelling. Available at: https://fennerschool-associated.anu.edu.au/mensuration/home.htm (Accessed: 3 October 2024).

Chan, L. et al. (2021) Handbook on the Singapore Index on Cities’ Biodiversity (also known as the City Biodiversity Index). Montreal and Singapore: Secretariat of the Convention on Biological Diversity and National Parks Board, Singapore. Available at: https://www.cbd.int/doc/publications/cbd-ts-98-en.pdf (Accessed: 25 September 2023).

Eldridge, D.J. et al. (2016) ‘Ecosystem structure, function, and composition in rangelands are negatively affected by livestock grazing’, Ecological Applications, 26(4), pp. 1273–1283. Available at: https://doi.org/10.1890/15-1234.

Eyre, T.J. et al. (2015) BioCondition: A Condition Assessment Framework for Terrestrial Biodiversity in Queensland. Brisbane: Queensland Herbarium, Department of Science, Information Technology, Innovation and Arts. Available at: https://www.qld.gov.au/__data/assets/pdf_file/0029/68726/biocondition-assessment-manual.pdf (Accessed: 13 October 2023).

Fensham, R.J. and Fairfax, R.J. (2008) ‘Water-remoteness for grazing relief in Australian arid-lands’, Biological Conservation, 141(6), pp. 1447–1460. Available at: https://doi.org/10.1016/j.biocon.2008.03.016.

French, R.J. (1987) ‘Future productivity on our farmlands’, in Proceedings of the 4th Australian Agronomy Conference. Lawes, QLD: Australian Society of Agronomy.

Global Reporting Initiative (GRI) (2018) GRI 303: Water and Effluents 2018. Amsterdam: Global Reporting Initiative (GRI).

Grill, G., Lehner, B., Thieme, M. et al. (2019). Mapping the world’s free-flowing rivers. Nature 569, 215–221. Available at: https://doi.org/10.1038/s41586-019-1111-9.

Hamlyn-Hill, F. (2011) Water Requirements for Cattle. Available at: https://futurebeef.com.au/resources/water-requirements/ (Accessed: 3 October 2024).

Hoekstra, A.Y., Mekonnen, M.M., Chapagain, A.K., Mathews, Z., and A. J. (2011) The Water Footprint Assessment Manual: Setting the Global Standard. London and Washington, D.C.: Earthscan. Available at: https://doi.org/10.4324/9781849775526.

Jaeger, J.A.G. (2000) ‘Landscape division, splitting index, and effective mesh size: new measures of landscape fragmentation’, Landscape Ecology, 15, pp. 115–130.

Keith, D.A., Jones, R., and D. S. (2020) IUCN Global Ecosystem Typology 2.0: Descriptive profiles for biomes and ecosystem functional groups. Gland, Switzerland: IUCN. Available at: https://doi.org/10.2305/iucn.ch.2020.13.en.

Luke, G.J. (1987) Consumption of water by livestock. Perth, WA: Department of Agriculture and Food, Government of Western Australia. Available at: https://library.dpird.wa.gov.au/cgi/viewcontent.cgi?article=1053&context=rmtr (Accessed 3 October 2024).

Natural Capital Coalition (2016) Natural Capital Protocol. London: Natural Capital Coalition. Available at:https://naturalcapitalcoalition.org/wp-content/uploads/2018/05/NCC_Protocol_WEB_2016-07-12-1.pdf (Accessed: 3 October 2024).

Pringle, H.J.R. and Landsberg, J. (2004) ‘Predicting the distribution of livestock grazing pressure in rangelands’, Austral Ecology, 29(1), pp. 31–39. Available at: https://doi.org/10.1111/j.1442-9993.2004.01363.x.

Sheldon, F. et al. (2012) ‘Identifying the spatial scale of land use that most strongly influences overall river ecosystem health score’, Ecological Applications, 22(8), pp. 2188–2203. Available at: https://doi.org/10.1890/11-1792.1.

Smith, G.S. et al. (2023) The Natural Capital Handbook: A practical guide to corporate natural capital accounting, assessment, risk assessment and reporting. Hobart: CSIRO. Available at: https://www.csiro.au/en/research/natural-environment/natural-resources/Natural-capital-accounting/Handbook (Accessed: 3 October 2024)

TNFD (2023) Recommendations of the Taskforce on Nature-related Financial Disclosures. Taskforce on Nature-related Financial Disclosures. Available at: https://tnfd.global/wp-content/uploads/2023/08/Recommendations_of_the_Taskforce_on_Nature-related_Financial_Disclosures_September_2023.pdf (Accessed: 3 October 2024).

Tongway, D.J. and Hindley, N.L. (2004) Landscape Function Analysis: Procedures for Monitoring and Assessing Landscapes. Canberra: CSIRO.

United Nation Environment (2017) A Framework for Freshwater Ecosystem Management. https://www.unep.org/resources/publication/framework-freshwater-ecosystem-management (Accessed: 3 October 2024).

United Nations (2021) System of Environmental-Economic Accounting – Ecosystem Accounting: White cover (pre-edited) version. New York, NY: United Nations. Available at: https://seea.un.org/sites/seea.un.org/files/documents/EA/seea_ea_white_cover_final.pdf (Accessed: 3 October 2024).

United Nations, European Union, Food and Agriculture Organization, International Monetary Fund, Organisation for Economic Co-operation and Development, and World Bank (2014) System of Environmental-Economic Accounting 2012 — Central Framework. New York, NY: United Nations. Available at: https://unstats.un.org/unsd/envaccounting/seeaRev/SEEA_CF_Final_en.pdf (Accessed: 3 October 2024).

Walker, S.J. et al. (2020) ‘A multi-resolution method to map and identify locations of future gully and channel incision’, Geomorphology, 358, p. 107115. Available at: https://doi.org/10.1016/j.geomorph.2020.107115

Wilkinson, S. et al. (2019) Gully and Stream Bank Toolbox. A technical guide for the Reef Trust Gully and Stream Bank Erosion Control Program. Second edition. Canberra: Commonwealth of Australia. Available at: https://www.dcceew.gov.au/sites/default/files/env/pages/661595d3-749f-4aef-9c4a-6e4d245ecc59/files/reef-trust-phase-iv-toolbox.pdf (Accessed: 16 March 2023).

Further Guidance

We recommend consulting the CSIRO Natural Capital Handbook (Smith et al., 2023).

Other key sources of guidance include

- SEEA Central Framework and Ecosystem Accounting online materials

- TNFD online materials

- Capitals Coalition online materials

- The Natural Capital Primer is a ‘one-stop shop’ for resources and information to learn about natural capital, explaining key concepts about natural capital in easy-to-understand language

- Nature Positive Matters is a network committed to making nature a priority in business decisions, driving positive change for our planet.

SEEA-CF Land Use classification

SEEA-CF 2014, Table 5.11

- Land

1.1 Agriculture

1.2 Forestry

1.3 Land used for aquaculture

1.4 Use of built-up and related areas

1.5 Land used for maintenance and restoration of environmental functions

1.6 Other uses of land not elsewhere classified

1.7 Land not in use - Inland waters

2.1 Inland waters used for aquaculture or holding facilities

2.2 Inland waters used for maintenance and restoration of environmental functions

2.3 Other uses of inland waters not elsewhere classified

2.4 Inland waters not in use

FAO Land Cover Classification System, version 3

- Cultivated and Managed Terrestrial Areas

- Natural and Semi-Natural Terrestrial Vegetation

- Cultivated Aquatic or Regularly Flooded Areas

- Natural and Semi-Natural Aquatic or Regularly Flooded Vegetation

- Artificial Surfaces and Associated Areas

- Bare Areas

- Artificial Waterbodies, Snow and Ice

- Natural Waterbodies, Snow and Ice